You don’t need to be rich to start investing. That is one of the most persistent and damaging myths in personal finance; the idea that investing is reserved for people with large sums of money sitting in a bank account. The truth is that in 2026, you can start building a real investment portfolio with as little as $100. The barrier to entry has never been lower, and the cost of waiting has never been higher. Now that you are aware about inflation it is the perfect time to discover the most elemental financial products with comissions as low as $0.

Why Starting Small Is Better Than Not Starting At All

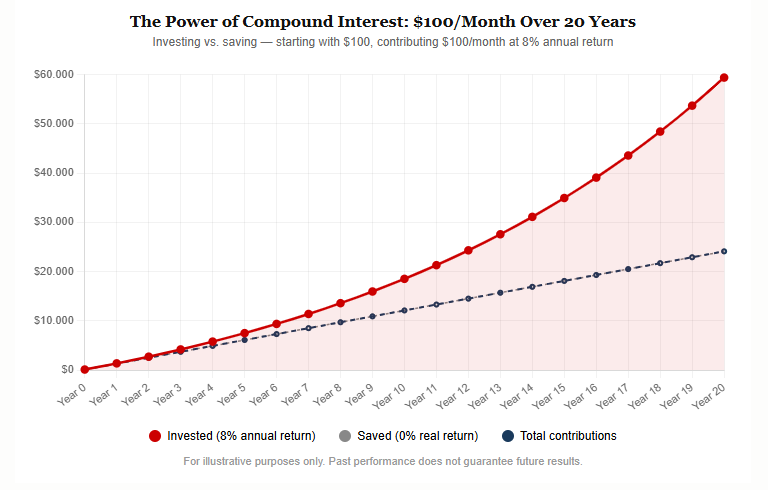

The most powerful force in investing is not how much money you have but it is time. Thanks to compound interest, even a small amount invested today grows exponentially over decades. A $100 investment that grows at 8% annually becomes $466 in 20 years without adding another cent. Add $100 every month and that same 20-year period produces over $58,000.

The math is unforgiving in both directions. Every year you delay starting is a year of compounding you never get back. This is why financial advisors universally agree: start as early as possible, even if the amount feels embarrassingly small.

What You Need Before You Invest Your First $100

Before putting any money into the market, three conditions should be met.

An emergency fund first. Your $100 should not be your last $100. Investing money you might need next month is not investing, it is gambling. Before investing, ensure you have at least one to three months of essential expenses saved in a liquid account and understand how inflation is eroding your money over time. If you don’t have that yet, build it first.

No high-interest debt. If you are carrying credit card debt at 20% interest, paying it down is mathematically a better return than almost any investment. Clear high-interest debt before investing.

A clear goal. Are you investing for retirement in 30 years? A house deposit in 5 years? Your child’s education? The time horizon determines the right strategy. Long-term goals can tolerate more risk. Short-term goals require more conservative approaches as short-term periods can be subject to higher market volatility because of black-swans (hihgly improbable events that alter significantly financial markets).

The Best Ways to Invest $100 in 2026

1. Index Funds and ETFs

This is where most beginners should start and where many experienced investors keep the majority of their money. An index fund is a collection of stocks that tracks a market index like the S&P 500. Instead of picking individual stocks, you buy a small piece of hundreds of companies at once.

The advantages are significant. They are low cost many have annual fees below 0.1%. They are diversified; one fund gives you exposure to hundreds of companies. And historically, index funds tracking the S&P 500 have delivered average annual returns of around 10% over long periods. Moreover, ETFs are one of the less time-consuming financial products which makes them suitable for the average investor.

With $100 you can buy fractional shares of funds like Vanguard’s VOO or BlackRock’s IVV through most modern investment platforms.

2. Fractional Shares

If you consider yourself a more engaged investor and believe you have the conviction to pick individual companies, fractional shares give you that flexibility without requiring large capital. Previously, buying a single share of Amazon, Google, or Tesla required hundreds or even thousands of dollars putting them out of reach for most retail investors. Today, platforms like Interactive Brokers, eToro, and others allow you to buy as little as $10 worth of any stock regardless of its share price. A $100 portfolio can hold positions in five or ten different companies simultaneously, giving you real diversification from day one. That said, stock picking requires research, discipline, and emotional resilience although it can be a great starting point for anyone who plans investing in the stock market for years.

3. Robo-Advisors

If you want a completely hands-off approach, robo-advisors are automated investment platforms that build and manage a diversified portfolio for you based on your risk tolerance and goals. They typically charge very low fees; often 0.25% per year and require minimal input from you beyond the initial setup.

Platforms like Betterment, Wealthfront, and others have no minimum investment requirements, making them ideal for beginners with $100.

4. High-Yield Savings Accounts and Money Market Funds

Not ready for market risk? A high-yield savings account or money market fund is a low-risk starting point. While returns are lower than equities; typically 4-5% in the current rate environment, your money is safe, liquid, and still earning far more than a standard savings account. Think of this as a stepping stone while you build your knowledge and confidence.

How to Choose the Right Platform

The platform you use matters. Look for these features:

- No minimum investment: essential for starting with $100

- Commission-free trading: most modern platforms offer this

- Fractional shares: allows full deployment of your $100

- Regulatory protection: ensure the platform is regulated in your jurisdiction

- Product catalogue: some brokers offer a larger catalogue or a more focused product range targeting different investors

In Europe, platforms like DEGIRO, Trading 212, and Interactive Brokers are popular regulated options. In the US, Fidelity, Charles Schwab, and Robinhood are widely used. Always verify that a platform is properly regulated before depositing money.

The $100 Investment Plan: A Simple Starting Template

Here is a straightforward allocation for a beginner investing $100 for the first time:

- $80 Broad market index fund (S&P 500 or global index ETF)

- $20 Individual stock of a company you know and believe in

This gives you diversified exposure through the index fund while allowing you to experience owning an individual stock which helps build interest and engagement with your portfolio.

As your contributions grow and your knowledge increases, gradually increasing the particular stock allocation can be considered. However, it is important keeping in mind that the more concentrated a portfolio is the higher the risks associated to it. Therefore investors should assess their tolerance to risk before making any allocation decision.

The Biggest Mistake Beginner Investors Make

Trying to time the market. Countless studies show that time in the market consistently beats timing the market. Investors who try to buy at the bottom and sell at the top almost always underperform those who simply invest consistently regardless of market conditions which is a strategy known as dollar-cost averaging.

“Time in the market beats timing the market”

With $100 a month invested consistently into a broad index fund, you are practicing dollar-cost averaging automatically. Some months you buy when prices are high, some when they are low but over time the average cost works in your favour. Moreover when prices are low those $100 can buy a bigger fraction of the share lowering the cost basis over the long-run.

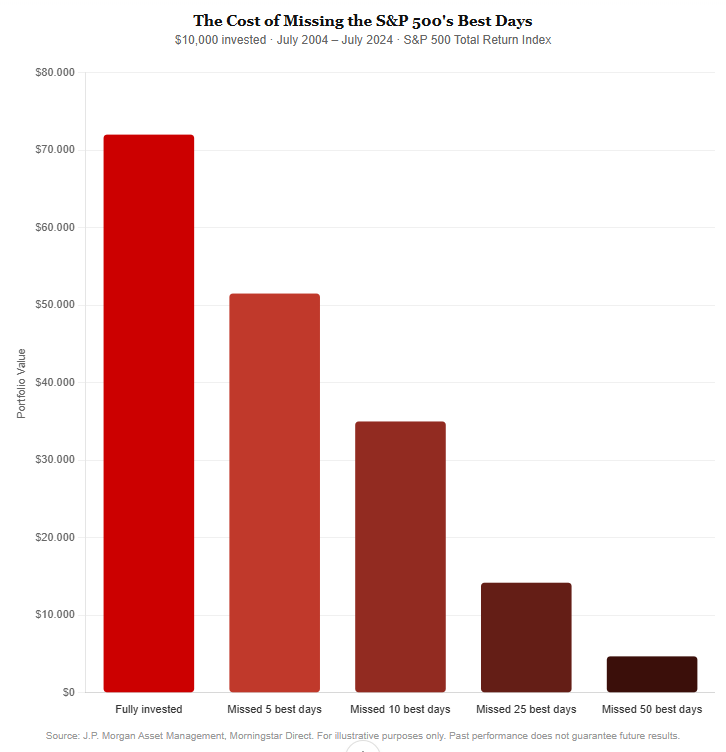

The numbers are brutal. A $10,000 investment in the S&P 500 from July 2004 through July 2024, left fully invested, would have grown to over $70,000; a 10.5% annual return. Miss just the 10 best trading days and that figure drops to under $35,000; miss 25 best days and you’re left with $14,200; miss 50 and you’ve actually lost money over 20 years.

Here’s the critical insight: over the last 20 years, seven of the 10 best days occurred within 15 days of the 10 worst days. This means that investors who panic-sell during crashes trying to avoid the pain almost always miss the explosive recovery days that follow. You cannot have one without the other.

The lesson is simple but psychologically difficult: stay invested, stay consistent, and let time do the work.

Key Takeaways

- You do not need large sums to start investing; $100 is enough to begin

- Time in the market is more important than the amount you invest

- Index funds and ETFs are the best starting point for most beginners

- Build an emergency fund and eliminate high-interest debt before investing

- Consistency matters more than timing; invest regularly regardless of market conditions

- Always use regulated, reputable platforms

es. Many modern investment platforms and apps allow you to start with as little as $1 through fractional shares, meaning you can own a small piece of expensive stocks like Apple or Amazon without needing thousands of dollars upfront.

For beginners, broad index funds or ETFs that track the S&P 500 are widely considered the safest starting point. They offer instant diversification across hundreds of companies, low fees, and have historically delivered strong long-term returns.

Investing is a long-term strategy. With consistent contributions and compound growth, small amounts can grow significantly over 10 to 20 years. The key is starting early and staying consistent rather than waiting until you have more money.

Popular beginner-friendly platforms include Fidelity, Charles Schwab, and eToro which all allow low or zero minimum deposits. Always research fees and features before choosing a platform suited to your country and goals.

Conclusion

The best investment you will ever make is the decision to start. $100 may feel insignificant today, but the habits, knowledge, and compounding returns it builds are anything but. Every major investor in history started somewhere and most will tell you their biggest regret was not starting sooner.